BizChina

- Details

- By David Cao

- Hits: 1476

Finnish mobile phone maker Nokia's move to provide a free navigation service in China is expected to boost the sale of navigation cellphones in the country, experts said.

Finnish mobile phone maker Nokia's move to provide a free navigation service in China is expected to boost the sale of navigation cellphones in the country, experts said.

That may also help Nokia maintain its dominant position in the country as users turn to CDMA and TD-SCDMA handsets, a market in which the Finnish firm does not have a significant presence.

Nokia Oyj, the world's biggest maker of mobile phones, said on Thursday that the company would offer the free navigation service on its Ovi Maps application in 74 countries and regions.

The company said about 20 million Nokia handset users could use the service right now, and it expects to sell 80 million navigation smartphone handsets globally in the next 18 months.

- Details

- By David Cao

- Hits: 1005

Guangzhou Automobile Group Co, the Chinese partner of Japanese car giants Toyota and Honda, plans to sell shares in Hong Kong, seeking foreign capital to boost its domestic expansion.

China's sixth-largest automaker will go public in Hong Kong through a backdoor listing using its Denway Motors unit, Denway said in a statement to the Hong Kong Stock Exchange on Friday.

However, the listing would not offer shares for public subscription, said Denway.

Denway shares, which doubled last year, jumped 7.58 percent to HK$4.97 (64 cents) in Hong Kong on Friday after the announcement and amid expectations Guangzhou Auto would pay a premium to take it private.

Guangzhou Auto now holds a 37.9 percent stake in Denway, a Hong Kong-based investment company controlling units and associates engaged in vehicle manufacturing and trading, according to the company's website.

- Details

- By David Cao

- Hits: 1054

The U.S. government will investigate charges against import of oil well drill pipe from Chinese companies, said the Commerce Department on Thursday.

The case, which was filed by the United Steelworkers union and a group of companies from Texas and Illinois, is the first U.S. trade probe of this year against China after about a dozen in 2009.

The petitioners have asked for anti-dumping duties ranging from 429 percent to 496 percent.

They also want additional countervailing duties to offset alleged government subsidies, the Commerce Department said.

The investigation covers heavyweight drill pipe and drill collars of iron or steel used to drill oil wells.

The Commerce Department said that the United States imported 194.6 million dollars worth of the drill pipe from China in 2008, up from 107.1 million dollars in 2006.

In this probe case, the U.S. International Trade Commission has to decide by mid-February whether there is a reasonable indication that U.S. companies have been injured or threatened with injury by the imports.

Read more: U.S. launches trade probe against Chinese drill pipe

- Details

- By David Cao

- Hits: 933

China's cruise economy kept growing as liner departures from and visits to Chinese harbors increased steadily in 2009, industry insider said Friday.

China Cruise and Yacht Industry Association told Xinhua Friday that China's cruise ship market will grow rapidly this year with liner visits expected to rise by a big margin. But it declined to reveal detailed predictions, only estimating that all-year cruise ship visits to Shanghai alone will reach 120 for 2010.

According to the association, cruise ship departures from China's coastal cities numbered 80 in 2009, a growth of 38 percent over the 2008 level; and cruise ship visits at such cities numbered 76. But the industry organization did not reveal the year-on-year change figure for the visits.

The association took Shanghai as an example. Last year the city recorded a 17-pecent year-on-year growth in number of international cruise ship visits and a 83-percent growth in number of human exits and entries by liners.

Read more: China to receive much more cruise ship visits this year

- Details

- By David Cao

- Hits: 1031

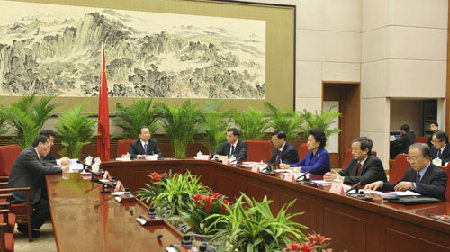

Chinese Premier Wen Jiabao (3rd L) presides over a plenary meeting of the State Council to discuss the draft of the government work report to be delivered at a national session of the country's parliament in Beijing, capital of China, Jan. 19, 2010.

Premier Wen Jiabao said Tuesday the acceleration of the adjustment of China's development pattern while maintaining steady and fast economic growth must run through all the government's work this year.

The government should incorporate speeding up the transformation of the development mode into maintaining steady and relatively fast economic development, Wen said at a plenary meeting of the State Council, or Cabinet.

At the meeting, a draft government work report, to be delivered at an annual national session of the country's parliament, was discussed.

The government must strengthen macro-economic control and carefully handle the relationship between maintaining steady and relatively fast economic development, adjusting economic structure and managing inflation expectations in a bid to create favorable conditions to transform the development mode, he said.

The government would stick to the policy of expanding domestic demand this year to boost public consumption and optimize the investment structure, he said.

Wen said the country should make "substantial progress" in transforming the economic development mode by continuing to push forward renovation of key industries, fostering strategic emerging industries, promoting accelerated development of the service sector, and improving the overall quality and competitiveness of the national economy.

The government would comprehensively implement its strategy of reinvigorating the country through science, education and expertise, and enhance its efforts to turn China into an innovation-oriented country so as to give technological and personnel support for the transformation of the development mode, he said.

The government should also make efforts to improve the people's living standards and deepen reforms of "key fields" to establish a system which was conducive to the transformation, he said.

More Articles …

Page 75 of 126